Data Center M&A On the Horizon as New SPACs Go Shopping

Data Center M&A On the Horizon as New SPACs Go Shopping

More investment dollars are targeting the digital infrastructure sector, signaling a new round of mergers and acquisitions (M&A) on the horizon.

News reports last week indicated there are two new special purpose acquisition corporations (SPACs) featuring teams of data center executives. Meanwhile, the industry’s busiest consolidator is raising a huge new round of capital.

Increased data center M&A was one of the trends DCF highlighted in our annual forecast, Eight Trends That Will Shape the Data Center Industry in 2021. The continued influx of investor capital is not a surprise, but the addition of multiple SPACs adds a new wrinkle to the trend, and is likely to boost the number of publicly-held companies focused on digital infrastructure.

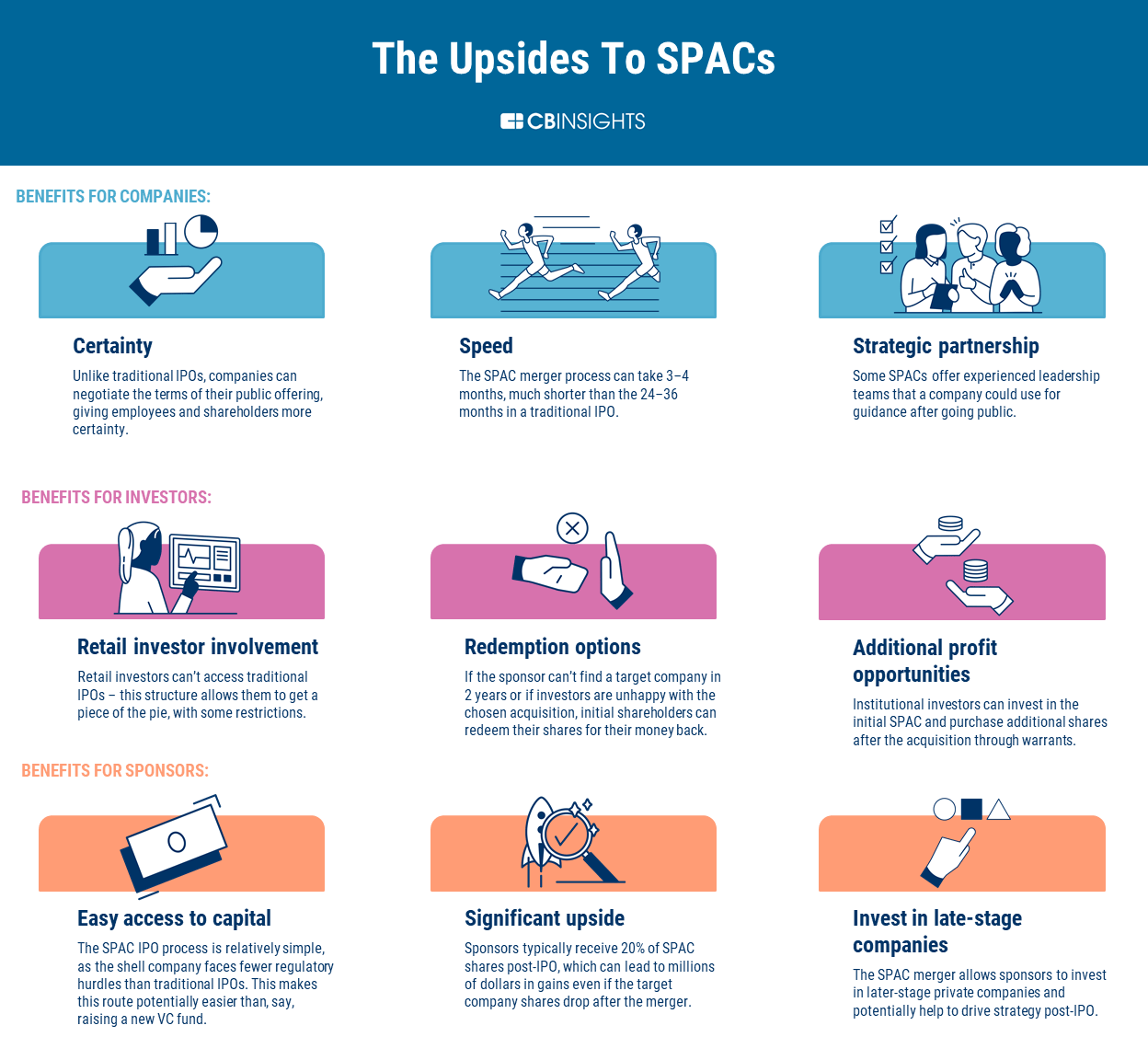

A SPAC is an investment vehicle that goes public and raises capital from investors for the purpose of acquiring a private company. An early example of the trend was the acquisition of Vertiv last year by GS Acquisition Holdings, a SPAC created by Goldman Sachs and veteran executive David Cote. Most SPACs are backed by an investment company and assemble a team of advisors and executives to manage the acquired property.

The deal positioned Vertiv as a public company focused on the growth of data center facilities, a “pure play” investment in a the hot digital infrastructure sector as huge investors race to meet the extraordinary demand for capital to fuel the shift to a data economy.

The two SPACs announced last week involve executives with lengthy history in the data center sector:

- Former CyrusOne Chief Technology Officer Kevin Timmons has joined the management team at InterPrivate Acquisition Partners, which Bloomberg reports is planning a SPAC targeting digital infrastructure. Former CyrusOne CEO Gary Wojtaszek and data center design pioneer Peter Gross are also working with InterPrivate as advisors. InterPrivate said its advisors and co-sponsors “bring deep sector expertise that make our SPACs attractive partners to potential merger targets, and act as credible validators to existing shareholders and prospective investors considering potential transactions. Certain of these individuals may also serve as Board members of target companies.”

- Michael Tobin, a serial entrepreneur in the data center sector, is reportedly working with an Amsterdam SPAC called Crystal Peak, Tobin is best known for his leadership of TelecityGroup, which was acquired by Equinix, and has held director or advisory roles at Leaseweb, Sungard Availability, IXCellerate, Chayora, DataPipe and Teraco Data.

Meanwhile, Colony Capital investment arm Digital Colony has reportedly raised more than $4 billion for its second fund dedicated to digital infrastructure, according to Bloomberg, citing a memo to investors. The fund is said to be seeking an additional $2 billion to support the ambitious growth strategy of Colony Capital, which operates DataBank and Vantage Data Centers as well as a family of companies spanning telecom towers, small cell and distributed antenna systems and fiber.

Colony wielded its previous $4 billion fund in a series of acquisitions that drove massive growth for Vantage Data Centers and DataBank. Vantage, which targets the wholesale and hyperscale data center market, expanded its IT capacity by 90 percent in 2020, while doubling the number of markets it serves. Colocation provider DataBank has become the platform for a series of acquisitions to implement Colony’s “digital playbook”, most notably the purchase of zColo data centers, which adding 44 data centers across 23 markets in the U.S. and Europe.

SPACs Offer New Exit Opportunities

The M&A scene has been active, with most of the major recent deals focused on global players adding capacity in new markets, especially Canada and Europe. Over the past two years we’ve seen new data center platforms backed by global investment giants, who may seek to gain scale through acquisitions.

The prospect of SPACs joining the fray provides additional exit options for privately-held data center companies, and could be especially attractive to those contemplating IPOs, as some analysts see selling to SPACs as a faster and more efficient path to the public markets than a traditional IPO. The SPAC route also offers more control over pricing on equity sales, as opposed to the last-minute, demand-based pricing for IPOs.

{kind=link}

With a growing pool of buyers and a dwindling pool of acquisition candidates, deal valuations seem likely to remain strong. Investors have been keenly interested in buying assets that benefit from the growth in hyperscale computing, especially in major markets like Northern Virginia. In a competitive bidding environment, new players may find opportunity in expanding their options to acquire companies operating in second-tier markets or adjacent technologies in power, cooling and automation software for data centers.

Marquee Investors Love Data Centers

As we noted last year, global investors are raising billions of dollars to invest in digital infrastructure, citing extraordinary demand for capital to fuel the data economy. Investment interest in data centers has been boosted by the growth of hyperscale computing, where the tenant is a giant corporation with excellent credit, lowering the risk profile for investors.

Here’s a look at some of the recent entries by well-heeled global investment firms:

- Goldman Sachs created Global Compute Infrastructure LP, a new data center development platform backed by $500 million from Goldman.

- GI Partners has lined up $1.8 billion in investor backing for its Data Infrastructure Fund and will fund digital infrastructure primarily in North America.

- KKR has formed Global Technical Realty (GTR) to develop more than $2.5 billion in data centers across Europe.

- Stonepeak Infrastructure announced the creation of Digital Edge to invest $1 billion in digital infrastructure across the Asia-Pacific region. Stonepeak also owns Cologix, a colocation and interconnection firm in North America.

- Bain Capital has taken Chindata Group Holdings public through a $540 million IPO on the NASDAQ.

- Macquarie Infrastructure Partners (MIP) has made a strategic investment in Aligned Energy to support the company’s growth, including expansion into new markets and supply chain innovation. Macquarie is also the majority owner of carrier hotel development specialist Netrality Data Centers.

- Brookfield Infrastructure Partners acquired Evoque Data Center Solutions, and hopes to be an active player in the global merger scene for digital infrastructure.

- Global infrastructure fund EQT Infrastructure has acquired EdgeConneX, which has been a leading player in both edge computing and hyperscale data center markets.

- Singapore’s sovereign wealth fund GIC has backed data center plays across three continents, including EdgeCore Internet Real Estate in the US and the Equinix xScale hyperscale initiative in Europe.

- Mubadala Investment Company, the sovereign wealth fund for the Emirate of Abu Dhabi, will invest $500 million to work with majority shareholder Stonepeak to support an ambitious growth strategy for Cologix.

- Global infrastructure investor Alinda Capital Partners is providing up to $1 billion in funding for future data center construction for QTS Data Centers.

- IPI Data Centers formed STACK Infrastructure with assets acquired from Infomart Data Centers and T5.

More >> Data Center M&A On the Horizon as New SPACs Go Shopping